Somehow mortgage rates went from being the best since 2022 to the worst this year, all in the span of about a week and change.

Talk about a rough stretch for mortgage rates, driven by the ongoing (and uncertain) conflict in the Middle East.

The long and the short of it is that oil prices have skyrocketed in response, leading to renewed inflation concerns.

When inflation is expected to get worse, the value of bonds (and mortgage-backed securities) erodes.

As a result, the yield (or interest rate) increases to offset the drop in price. And that’s why mortgage rates are the highest they’ve been all year.

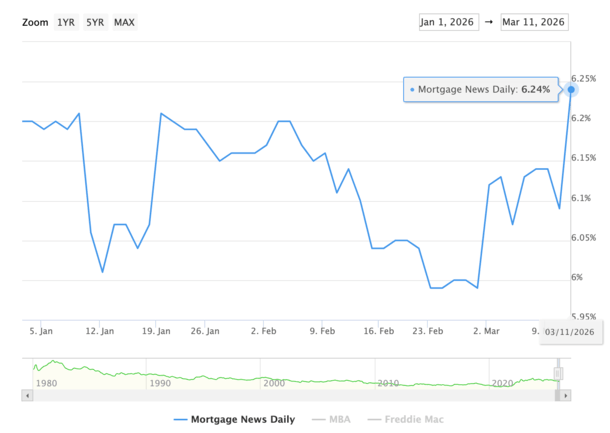

Mortgage Rates Hit Highest Point of the Year

Things were looking really good for mortgage rates through the first two months of the year.

The 30-year fixed hit its lowest point since around late summer of 2022.

Two weeks ago, Freddie Mac reported that the popular mortgage hit its lowest point in 3.5 years, averaging 5.98% according to their lender survey.

A week later it had climbed back into the sixes, but to 6.00% exactly, which was still an attractive rate.

Tomorrow they’ll release their next weekly survey, but it probably won’t capture all the upward movement seen in the past 24 hours.

The daily updated rate index from Mortgage News Daily initially rose to 6.19% this morning, then got an unfavorable midday re-price to 6.24%.

That puts it four basis points above the prior 2026 high of 6.21%, per MND.

The good news is we’re still talking about a handful of basis points, which aren’t a lot.

In fact, the interest rate might be the same but simply cost a little more at closing.

And the monthly payment probably isn’t much different at 6.25% versus 6%.

On a $500,000 loan, it’s actually only a difference of $80 per month in principal and interest.

But to the prospective home buyer, it might look and feel a lot worse.

I keep talking about this and it’s hugely important. It’s all about buyer psychology.

If you go buy a big screen TV and the price was $999 but is now $1,075, you’re going to feel like you got a raw deal.

You might still go through with it, but it’s going to rub you the wrong way.

Now imagine a mortgage, where that higher rate stares at you each month for potentially the next decade or longer.

Not a great feeling and obviously it costs you more money too!

How Bad Can Mortgage Rates Get, Again?

As I’m writing this, I’m thinking of those annoying 7% mortgage rates again that kept re-emerging time and time again these past few years.

We seemed to finally shake those last spring and hopefully they don’t return anytime soon.

I don’t think it gets quite that bad because at a certain point persistently expensive oil prices would likely usher in a recession. Woo hoo!

And you’d think we’d get lower bond yields if that were the case, as the 10-year tends to fall during downturns.

However, we could see 30-year fixed mortgage rates continue to rise if the current situation deteriorates and there’s not the usual flight to safety because of oil prices.

In other words, in the near term we could see the 30-year mortgage jump back toward 6.50%, while maintaining upward pressure and a resistance to fall back to recent levels.

Remember, rates take longer to fall than they do to rise. So once they go up, they can get stuck there for a while.

Crucially, this is happening during peak home buying season, meaning they might not be able to return to those tasty 5-handle levels until perhaps after summer at this point.

(photo: Topher McCulloch)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.