While last year was the worst year since the GFC in terms of home price growth, 2026 is slated to be another typical UP year for the housing market.

Some outlets like Redfin have already referred to it as the “Great Housing Reset,” expecting price normalization as housing affordability finally improves.

Long story short, incomes are expected to outpace home price gains, and coupled with lower mortgage rates, the housing market can begin to heal.

But that’s interesting is home prices didn’t appear to go down much despite the mortgage rate shock of the past few years.

And the year 2025 was reportedly the worst year for home prices since the GFC, but is now apparently behind us.

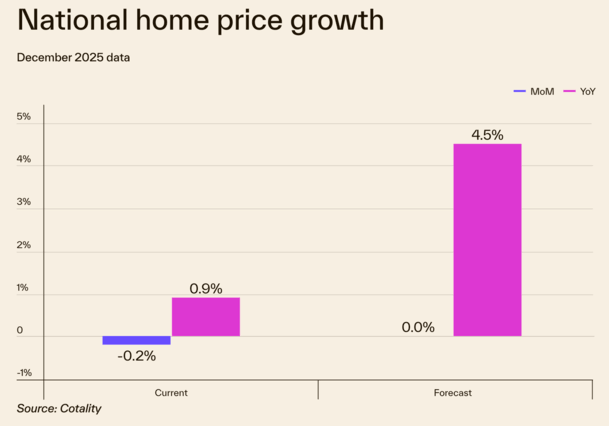

Home Prices Rose Less Than 1% in 2025

First things first. Home prices increased just 0.9% from December 2024 to December 2025, per the latest report from Cotality (formerly CoreLogic).

The company pointed out that it was “one of the softest rates since the post-Great Recession recovery.”

I dig some digging to ballpark home price gains since the prior cycle peak in 2006 and found it to be true.

This is what annual home price growth looked like based on my findings:

2025: ~1% (lowest since GFC recovery)

2024: ~4–6%

2023: ~5–6%

2022: ~6–11%

2021: ~18–19%

2020: ~6–11%

2019: ~5%

2018: ~5–6%

2017: ~6–7%

2016: ~5%

2015: ~5%

2014: ~4–5%

2013: ~7–8%

2012: ~3–5%

As you can see, home prices increased every year since 2012. It’s been a nice run.

The year 2012 was the first winning year for the housing market post-GFC.

Prior to that, home prices fell every year from 2007 through 2011 before recovering.

And as stated, they peaked around mid-2006 before the crash began.

Last year marked the worst year since, though prices still eked out a small gain.

Home Prices Expected to Rise Nearly 5% in 2026

But now it appears to be business as usual for the housing market again, with Cotality forecasting a 4.5% rise in home prices this year (from Dec. 2025 – Dec. 2026).

That would be squarely in line with the typical annual gain in home prices between 3-5%.

So does that mean the housing market already hit rock bottom this cycle? That 2025 was the crash?

Or at least the worst year this cycle and the worst since the GFC. And with home prices now expected to rise again, that the worst is behind us?

I probably wouldn’t get too far ahead of myself here nor would I just take the forecast at face value without a grain of salt.

But it is possible that we see home prices turn higher again, home sales volume increase, and affordability improve.

Just note that this recovery “will depend heavily on wage growth and how soon buyers regain the purchasing power needed to meet sellers’ pricing thresholds, per Cotality chief economist Dr. Selma Hepp.

In other words, if we see more layoffs and a higher unemployment rate, things could go sideways (or actually down).

There are a lot of unknowns related to AI and how that might shake out for the workforce.

It May Depend on the City and State In Question

In addition, home price gains (or losses) will depend upon the specific market in question.

Remember, real estate is local and not all markets are winning or losing right now.

Per Cotality, the states of New Jersey (+5.5%), Illinois (+5.4%), Nebraska (+5.4%), and Connecticut (+5.1%) have been the strongest home price performers over the past year, generally due to a lack of existing inventory and affordable prices.

Meanwhile, we’ve seen negative home price growth in many Southern and Western states, including Arizona, California, Colorado, Florida, and Texas.

Although there are some encouraging signs in those states as well with inventory dropping in places like Florida, possibly leading to price stabilization this year.

So is the worst behind us already? Is that even possible? Is it inevitable that we’ll experience another major housing crash?

Hard to know, but expecting another 2008-style housing crash in the immediate next cycle seems unlikely.

Given how rare the 2008 crash was, experiencing another one right after would be surprising.

Read on: Here’s Why the Housing Market Isn’t Crashing Today

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.