One silver lining to elevated mortgage rates, other than the refinance opportunity later, has been a shifting psychology.

A few years ago, I wrote that your brain (and my brain and everyone else’s) would soon think a 5% mortgage rate is pretty good.

That was prior to mortgage rates going even higher, cresting at around 8% and then coming back down to earth (a bit).

The logic was that after seeing higher, you might forget about lower and come to terms with something in between being not so bad.

Now, your brain might think the same of a 6% mortgage rate.

A 6% Mortgage Rate Doesn’t Look Too Bad Anymore

The higher-for-longer mortgage rate environment has lasted longer than most imagined, including myself.

And it might persist even longer than that. Nobody knows for sure. We make educated guesses and are often wrong.

A lot of pundits expected the 30-year fixed to fall closer to 6% by the end of 2025, including myself.

That’s still in play as it’s still only May, and we’re technically not that far away. But we still need something to drive rates lower.

Lately, there’s been nothing but headwinds, whether it’s tariffs, a global trade war, and the latest, a credit rating downgrade of the United States.

However, underneath all the headlines the economic data is showing more and more signs of cooling. And ultimately that’s what dictates the direction of mortgage rates.

The rest is a sideshow and something to banter about from day to day.

Anyway, I got to thinking lately that the so-called magic number for mortgage rates has risen, perhaps in light of these higher-for-longer rates.

In the past, it may have been 5%. At some point a year or so ago, it was said to be 5.5%.

Today it might be 6%, or anything on the better side of 6.50%, e.g. 6.49% and below.

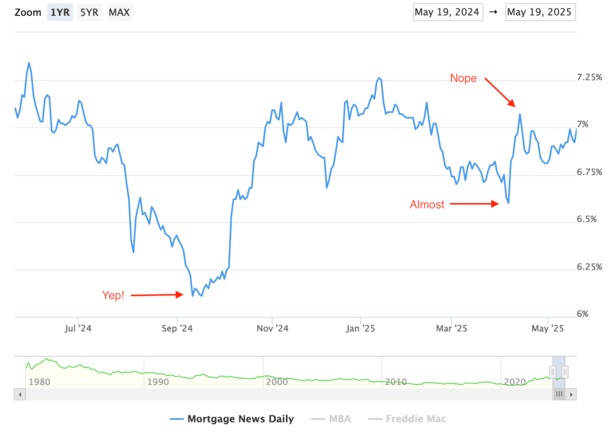

Just looking at this chart from MND over the past year, there have been two periods where rates got to those levels.

During those times, the housing market seemed to get a pep in its step, and mortgage refinancing also got a huge boost.

So maybe just maybe the answer for prospective home buyers (and some existing homeowners looking for rate relief) isn’t all that far off.

Coming to Terms with Higher for Longer

Gone are the days of hoping you can simply date the rate and marry the house.

Those who thought they could probably have a much higher mortgage rate than anticipated today.

Of course, they might have something below current market rates the way things went over the past few years.

For example, someone may have purchased a home with a 5.5% mortgage rate, expecting to hold it only temporarily.

But in retrospect, their 5.5% rate doesn’t look so bad anymore. It’s a “good rate” all things considered.

This is the same psychology I’m talking about with prospective home buyers today. Their mindset may have changed regarding what’s good and what’s bad.

And as time goes on with higher-for-longer rates, that number they’re comfortable with appears to be climbing as well.

Simply put, the longer we have these 7% mortgage rates, the better things will look if/when rates come down a bit.

The Mortgage Math Still Needs to Pencil

But there’s a caveat. You might be more comfortable with a higher mortgage rate today because you’ve grown accustomed to seeing them.

However, you still need to qualify for the mortgage at the higher rate. So it’s one thing to think, “Hey, it’s not so bad.”

And another to actually keep your debt-to-income ratio (DTI) below the maximum threshold.

There’s also the matter of finding a suitable property that remains in budget, despite the higher rates on offer.

This could require some concessions on the side of the home seller, whether it’s a price cut or seller concessions that can be used for buying down the mortgage rate.

For the record, this is a handy tool for today’s home seller to pitch to buyers. If they offer some credits toward closing, they can be used to pay for discount points.

These discount points are a form of prepaid interest that can lower the mortgage rate for the life of the loan.

And that’s one way to get to your own “magic number” without needing mortgage rates to fall.

An alternative is using concessions to create a temporary buydown fund where payments are lower for the first year or two.

But that would require some action on your part, a rate and term refinance eventually, assuming you want a permanently lower payment.

The point is we don’t appear to be too far off when it comes to mortgage rates, with action picking up when rates get closer to 6% than 7%.

And given many of the 2025 mortgage rate forecasts have rates falling toward those levels, relief could be in sight.

Just mind the rest of the economy, which is looking a little shaky of late.

(photo: Chris Hsia)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.