Ontario saw a 5.3% drop in consumer insolvency filings in April compared to the same time last year, according to new data from the Office of the Superintendent of Bankruptcy.

While that may appear positive on the surface, some experts warn it’s not necessarily a sign of recovery.

Recent data from insolvency firm Hoyes Michalos suggests many Ontario households are still under significant financial stress, particularly those with mortgages.

In their latest Homeowners Bankruptcy Index, Hoyes Michalos reported a rise to 8.5% in May, highlighting growing pressure on borrowers struggling with high-interest debt and housing costs.

Consumer proposals rise as borrowers look to avoid bankruptcy

Ontario’s year-over-year drop in insolvency filings contrasts with other signs of growing consumer stress. Credit card debt remains elevated, with Equifax, with Equifax recently reporting that 1.4 million consumers missed a credit payment in Q1.

Similarly, reliance on consumer credit is growing across Canada, particularly among younger borrowers and in regions with high mortgage costs.

In response to mounting debt pressures, an increasing number of Canadians are opting for consumer proposals over bankruptcies.

In April, consumer proposals made up 77.3% of all filings across Canada, with 80.6% in Ontario. This may suggest that more Canadians are seeking to restructure their debts without surrendering assets, but are still in need of formal relief for unmanageable debt levels.

While the April decline may appear encouraging, according to Hoyes Michalos it does not reflect a meaningful easing of household strain.

“The slowing in growth should not be interpreted as improving financial health among Canadians,” the firm noted. “Rather, it is an indicator that households are simply holding on a little longer.”

Mortgage holders under strain

Even as filings eased in April, the overall stress on mortgage-carrying households continues to build.

The Hoyes Michalos Homeowners Bankruptcy Index rose to 8.5% in May, a 3.2% year-over-year increase and one of its highest readings in recent years. The index tracks the share of insolvent debtors who own a home, and the latest uptick highlights growing pressure on borrowers juggling high-interest debt alongside their mortgage.

“Homeowners filing insolvency in Canada are not necessarily delinquent on their mortgages. The problem is the amount of unsecured debt they carry on top of their mortgage,” Hoyes Michalos noted in its monthly briefing.

According to the firm, the average insolvent homeowner currently owes an additional $72,510 in unsecured debt, on top of their mortgage debt.

For many, it’s not the mortgage itself that triggers insolvency, rather the compounding effect of credit card balances, personal loans and other unsecured borrowing layered on top of housing costs.

Those most vulnerable to insolvency include landlords with multiple properties who are struggling to manage their mortgage payments, as well as pre-construction buyers facing challenges closing as planned. Falling property values, rising interest rates and construction delays are all contributing factors.

Short-term relief masks long-term risks in national insolvency trends

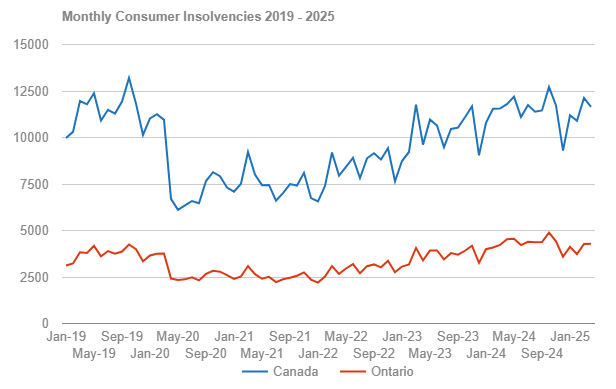

Nationally, April’s insolvency rate paints a mixed picture.

The total number of insolvencies in Canada fell by 3.7% from March and was down 1.8% year-over-year. But while that may suggest a brief reprieve, the broader trend points to mounting pressure on Canadian households.

Source: Office of the Superintendent of Bankruptcy

Over the 12-month period ending April 2025, consumer insolvencies have risen by 6.1%, with both bankruptcies and proposals trending upward.

While consumer proposals made up the vast majority of filings, their share dropped slightly to 78.7%, down from 79.0% the year before.

The trend was similar in Ontario where, despite a 5.2% year-over-year drop in April filings, the province’s insolvency count remains elevated over the long term. Ontario proposal rates sit even higher than the national average at 80.6%.

According to Hoyes Michalos, the combination of rising interest rates, falling home prices, credit tightening and increased unemployment are fundamental factors that lead to an increased chance of insolvency for homeowners.

“Given these persistent headwinds, we continue to predict consumer insolvencies will increase toward the later half of 2025,” Hoyes Michalos noted.

Visited 72 times, 72 visit(s) today

bankruptcies consumer insolvencies Homeowners Bankruptcy Index Hoyes Michalos insolvencies steven brennan

Last modified: June 26, 2025